As affordability continues to shape the housing market in 2026, lenders are expanding solutions to meet evolving borrower needs. Primary Residential Mortgage, Inc. (PRMI) is responding to this demand by

supporting financing options for manufactured and modular homes located within mobile home parks, also known as leased land communities.

This expansion represents an important step forward in providing access to attainable homeownership opportunities for a broader range of qualified borrowers.

Mobile Home Parks and Leased Land

Historically, many mortgage programs including those commonly offered across the industry have been primarily structured for manufactured homes affixed to privately owned land, allowing them to be financed as real property.

Manufactured homes located in mobile home parks, where the borrower owns the home but leases the land have traditionally required alternative financing structures. In these cases, the home is often treated as personal property rather than real estate, which can limit eligibility for certain loan programs.

With the expansion of lending guidelines and increased focus on affordable housing, financing solutions are becoming more accessible for these property types. Manufactured housing communities play a vital role in the U.S. housing landscape. These communities typically operate under a model where:

- The homeowner owns the manufactured or modular home

- The land is leased through a lot rent agreement

- The Community provides infrastructure & Shared amenities

- Available in several USA states

“We want the people to be aware of their funding options and resources to help maintain stability and security in a constantly evolving financial landscape.”

– Shellie Robinson, CEO of World Trust Media Network

These housing options offer a more cost-effective alternative to traditional site-built homes, helping meet housing needs in both rural and suburban markets.

Manufactured housing also continues to be supported by broader housing initiatives as a key affordability solution.

Access to Affordable Housing

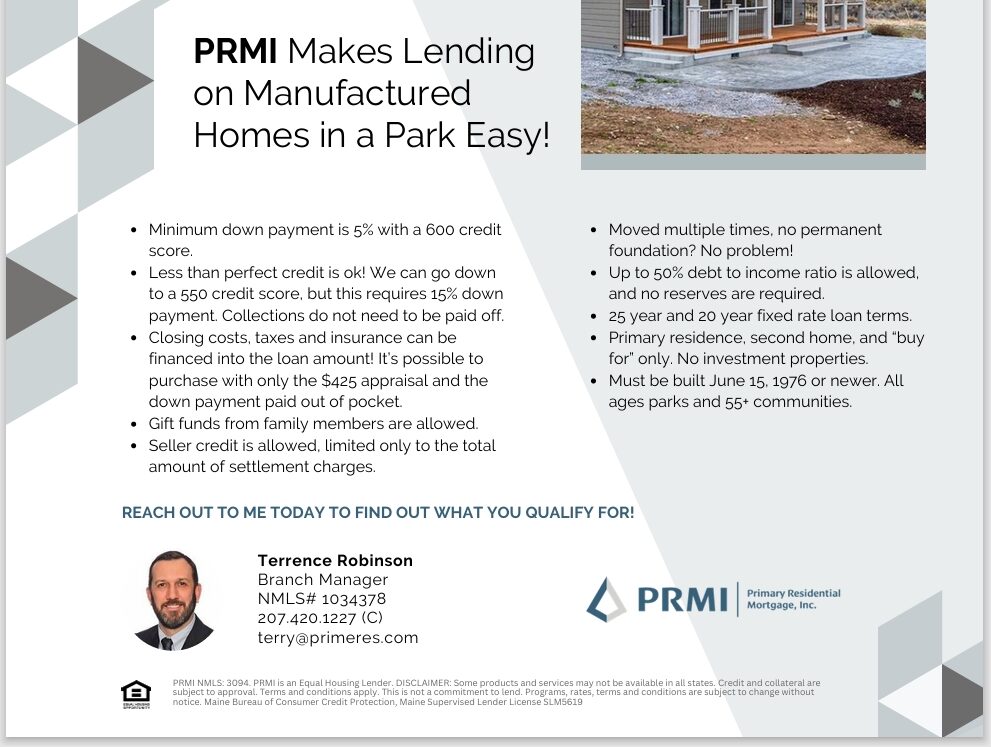

PRMI Makes Lending on Manufactured Homes in a Park Easy! Their alignment with this segment of the market reflects a broader industry commitment to expanding housing accessibility. With Greater access to homeownership for borrowers who may not be purchasing land, this greatly lowers the initial cost of new home construction versus on site stick-built homes. Opportunities to purchase existing-mobile homes increase availability of financing solutions in markets where inventory is limited.

Program availability, eligibility, and loan structure may vary based on borrower qualifications, property characteristics, and applicable guidelines.

What This Means for Borrowers

Having less than perfect credit is ok! Primary can go down to a 550 credit score, but this requires 15% down payment. A 600 credit score is their minimum with a 5% down payment of the mobile home purchase price. It gets even better, to help with America’s struggling economy, PRMI doesn’t require collections to be paid off. Closing costs, taxes and insurance can be financed into the loan amount! It’s completely possible to purchase with only the appraisal fees and the down payment.

Particularly those purchasing homes within mobile home parks, many now have additional pathways to financing, subject to applicable guidelines.